6 ways for off-grid companies to lower the costs of quality Solar Home Systems

Pricing quality: Cost drivers and value add in the off-grid solar sector

Non-quality verified offgrid solar products have a market share of about 71 %. Healthy competition is good for customers, but a race to the bottom will not serve anyone. This report identifies strategies to reduce the cost of solar products without compromising on quality and informs policymakers of opportunities to promote affordable, quality products to off-grid and poor-grid families.

Quality Off-Grid Solar (OGS) products often cost 2-5 times the price of non-quality products

Today, 434 million households live off-grid or in poor-grid regions. Responding to this need, the off-grid industry has developed various types of products in the last 10 years and now provides energy access to 108 million people.

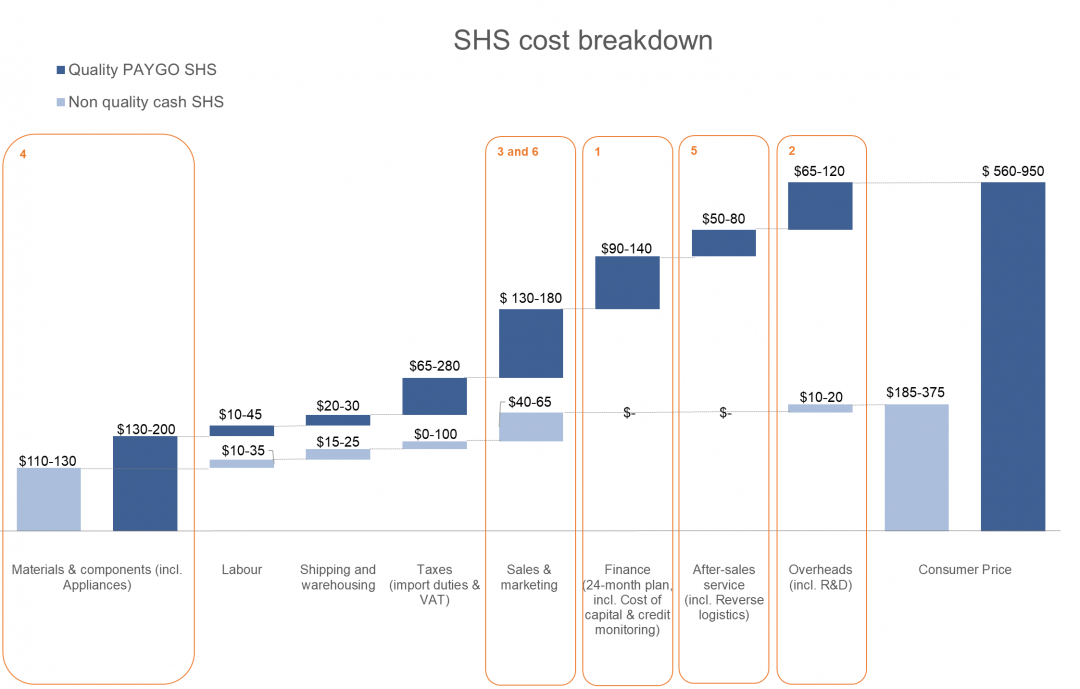

If the expansion of the off-grid sector improves access to energy, the proliferation of different products types has increased competition, pushing producers to lower their prices and in some cases compromise on the quality of the products distributed. Quality manufacturers and distributors exist, and they invest in the customer experience to gain trust and deliver impact, yet today 71% of the market is constituted by non-quality verified (non-QV) products. These can be 4-5 times cheaper than quality items, but they do not meet international or national quality standards. The “Quality Matters” study, conducted by Lighting Global (LG), indeed found that all 17 tested top-selling non-quality verified (non-QV) solar products sold in five markets across Africa and South Asia failed to meet the LG quality standards for pico-PV products, and were more likely to have deficiencies that resulted in a shorter lifespan.

Poor quality can be detrimental both for end-users and producers. Consumers miss out on the promised benefit that they paid for, and often end-up paying more to replace defective products than what they would have otherwise paid for a higher quality product. Companies suffer from the lack of customer confidence, which has a detrimental effect on demand. If healthy competition encourages a dynamic sector growth, a race to the bottom that fails to deliver customer value and satisfaction is not serving anyone.

In our recent report “Pricing Quality: Cost drivers and value add in the off-grid solar sector” sponsored by IBAN, we have tried to understand where this price difference comes from, as summarized in the graph below.

These analyses are indicative of trends, not reflective of a given product or country. They also do not reflect the wide variations in both quality and price points that exist within each of the quality and non-quality categories. Yet, they provide validated insights into why quality costs more, based on Hystra's ten years of experience in the sector (which includes in-depth analysis of dozens of energy players) and on GOGLA’s knowledge of their members. Hypothesis were further pressure-tested with 15+ OGS companies and experts.

This article proposes six possible avenues for quality OGS companies to reduce the price difference of their products compared to non-quality products, starting from the cost categories that account for most of the price difference between quality and non-quality Solar Home Systems (SHS). These are not the only solutions, but they are a start!

6 possible avenues that could allow quality players to reduce costs

1. USE INNOVATIVE FINANCING SUCH AS CROWDFUNDING TO LOWER COSTS OF END-USER FINANCING

Financing costs account on average for 24% of the price difference between quality solar home systems sold with PAYGO credit scheme, and over the counter SHS. Since in most cases only quality product companies offer customer financing mechanisms, financing is a key driver of the price difference between QV and non-QV products. One of the reasons for these costs is that access to acceptably priced refinancing lines remains a key challenge for distributors: a recent study of 72 small last mile distributors, including 59% selling solar products, found that over 75% of them cited access to finance as a key barrier to growth. Debt is particularly hard to access, a main reason being that collateral requirements are too hard to meet (cited by 27 per cent of surveyed last-mile distributors that tried to raise debt): companies’ main physical asset, namely their stock, is unattractive as a form of collateral since it cannot be easily sold to recover funds. And PAYGO companies need a lot of debt to fund their credit schemes, as it takes them over a year to recoup customer’s payments. Ultimately, low availability of acceptably priced debt affects the consumer which is charged a high interest rates as part of the monthly PAYGO fees to compensate for the high interest rates at which distributors must borrow. Innovative financing mechanisms are key to lower the cost of borrowing, and hence end-user financing. An effective way to raise cheaper debt has proven to be crowdfunding platforms. For small last mile distributors, crowdfunding is actually one of the most common source of debt.

BBOX, a solar-home-systems producer selling products in more than 35 countries, has recently raised $ 1m in the form of a loan thanks to the crowd funding campaign conducted on Trine. In order to attract investors, BBOX has used receivables as a creative form of collateral, i.e. the funds the company can expect to receive from PAYG customers in future.

2. THINK TWICE ABOUT WHERE TO LOCATE HEADQUARTERS AND WHO YOU NEED AT HEAD OFFICE

Overheads costs account on average for 19% of the price difference between quality and non-quality products. Some of these overheads represent investments in R&D that quality companies make – while many non-quality companies simply copy popular designs. Beyond R&D, an important part of the gap is driven by the fact that a significant number of early entrants have Western founders and established their headquarters back in their founders’ originating countries. “Remote from the field” headquarters sometimes remains relevant for fundraising purposes. However, as competition is getting fiercer, these companies — mostly quality players — are disadvantaged by the resulting expensive overheads needed to pay for headquarters and for expatriates’ wages on the ground. As a solution, a number of companies is choosing to hire more local staff and reduce their headquarters’ headcount significantly in developing countries, relocating staff to regional headquarters and offices.

Nadji.Bi, an African manufacturer of productive and smart solar solutions, has chosen to locate its headquarters in Mbour, a secondary city in Senegal. This has allowed them to contain headquarters cost compared to possible Western alternatives. Local headquarters have in addition proven to be an asset for branding and business development.

3. SET UP INNOVATIVE COLLABORATIONS FOR SALES AND MARKETING

Sales and marketing costs explain on average 21% of the price difference between quality and non-quality products. For SHS, the differential is mainly due to the costs of bringing solar products to the last mile. While in theory marketing and distribution costs should not be dependent on quality, it is mainly quality players that invest in costly proprietary distribution networks to reach rural areas and that more generally open new markets and invest in creating awareness around solar products. Instead, non-quality players mostly focus on urban or peri-urban areas and often are followers in these markets, limiting themselves to over the counter marketing while benefitting from the consumer awareness efforts made by their quality competitors. To lower sales and marketing cost, quality manufacturers and distributors could work collaboratively to leverage synergies in marketing and sales.

In Nigeria, Lumos Global established a partnership with MTN, the leading ICT company in Nigeria, to reach off-grid customers in rural areas by displaying solar products at MTN service points. Similarly, Fenix International partnered with MTN in Uganda to leverage its shop network.

4. INVEST IN PRODUCT DESIGN INNOVATION TO REDUCE THE QUANTITY AND PRICE OF COMPONENTS REQUIRED

While components and material costs have decreased steeply in the past ten years and will continue to do so thanks to fast technological development, they still represent the largest cost incurred by manufacturers and account on average for 9% of the price difference between quality and non-quality products. Cheaper components compromise product quality: the batteries of non-QV products have been found not to meet storage durability and to have deep discharge and overcharge protection issues. To reduce the price premium associated with quality components, manufacturers could invest in product design innovation that helps reduce the amount of materials used in a given product.

Renewit is an off-grid solar manufacturer selling hundreds of thousands of units per year. Richard Atwal, its managing director, identifies the company’s 20-year expertise in “design for manufacturing” as a key factor to drive costs down. Renewit often realizes that initial product designs sent by its clients are not cost-effective, and helps them save up to 25% on materials and assembly. Adjustments include for example making all the electronic components fit on one board and reducing the number of raw materials used. In addition to generating direct savings, such optimization also helps reduce the size of products and the corresponding shipping costs.

5. CONSIDER SHARING AFTER-SALES SERVICE WITH OTHER PLAYERS TO REDUCE AFTER-SALES COSTS

After-sales service is a key differentiating point between quality and basic off-grid solar products, representing on average 14% of the price premium. The difference is driven by the fact that non-QV products are often sold at the counter with no (enforced) product insurance or after-sales service: among the non-QV products tested in the “Quality matters” report, 88% did not include a consumer-facing warranty. One way to reduce the cost of after-sales is to delegate the task to a service provider. A separate entity would be able to serve different manufacturers and distribute the costs among them.

Sollatek, a thirty-five-year-old distributor of innovative energy products, is setting up a pilot to develop such a centralized service in East Africa with the support of the Global Distributors Collective. They are planning to procure products from multiple companies, stock them in a centralized in-country warehouse and distribute the replacements to local electronic shops which can conduct simple repairs in loco or send products to be replaced at the centralized warehouse. These centers would not only allow to leverage economies of scale, reducing the cost of after-sales, but are also expected to shorten the time to repair products from 3-6 months down to a couple of weeks.

6. COLLABORATE WITH PUBLIC ACTORS TO ALLOCATE INVESTMENTS STRATEGICALLY

The interests of policymakers and off-grid solar players clearly converge towards bringing power to as many people as possible. As a consequence, they have a clear interest in collaborating on how to tap into off-grid households’ significant needs. This can start by making the right and accurate data available. This goes both ways: off-grid solar players could offer PAYGO data (which can help extract whole communities from statistical void) while governments could share public grid expansion plans and any information that can help assess customers’ ability to pay. Such data would help inform the development strategy of OGS players who in turn can allocate their investment more wisely, be it towards rural areas with long-term potential or towards markets where quality products are endorsed by relevant authorities which hence require lower marketing costs.

Some companies have started using the database of potential SHS communities which the government’s Rural Electrification Agency has made publicly available. They have found the database has allowed them to make more informed decisions concerning which geographical areas to target.

There are other important lessons learnt for OGS companies to succeed, that go beyond the scope of how to reduce product price. Some can be found in SolarNow founder Willem Nolens’ article in response to this blog post - where he shares alternative ideas about the cost reduction proposed above, as well as additional tips on running a successful OGS company.

For more information on the cost drivers that explain the differences between quality and non-quality solar products, see the full report “Pricing Quality: Cost drivers and value add in the off-grid solar sector” published in Dec 2019.